Your 20s are the phase where you start earning, spending, and making financial decisions on your own. What you do with your money now can shape your future in a big way.

Your 20s are the phase where you start earning, spending, and making financial decisions on your own. What you do with your money now can shape your future in a big way.

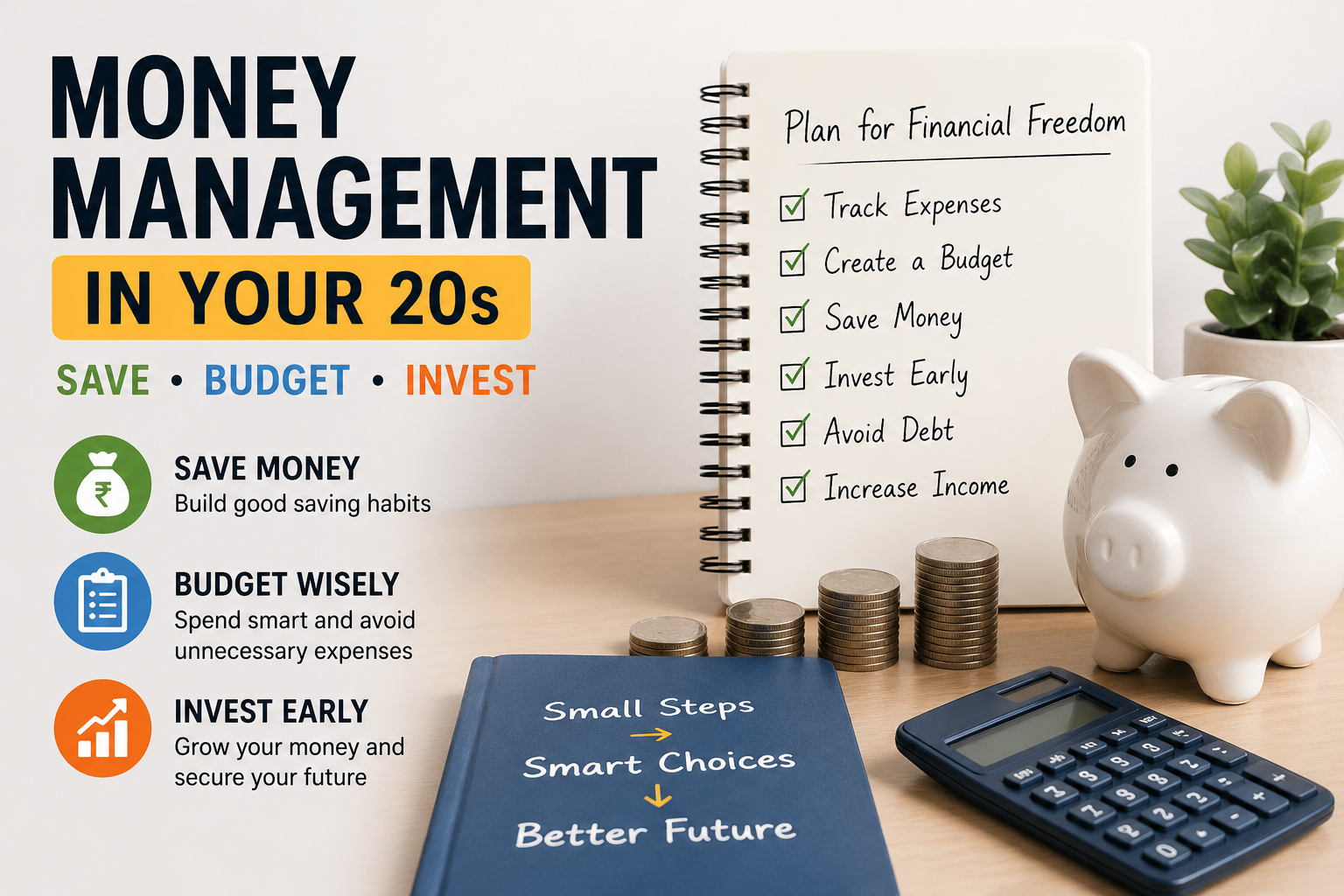

A lot of people in their 20s end up spending more than they should, saving very little, and relying too much on credit. It’s a common pattern. But managing money doesn’t mean you need a high salary — it just means you need some basic discipline and a clear plan.

In this guide, you’ll see how to handle your money better, even if your income is limited.

Why Money Management Matters in Your 20s

When you start early, you give yourself more time. And in finance, time matters a lot.

For example, even a small amount like ₹1,000 invested every month can grow into something meaningful over the years. That’s because of compounding — your money starts earning on itself.

Managing money properly also helps you stay out of unnecessary debt, deal with unexpected expenses, and slowly move towards financial independence.

Step 1: Track Your Income and Expenses

Before changing anything, you need to know where your money is going.

Start by writing down:

- How much you earn every month

- Your fixed expenses like rent and bills

- Your day-to-day spending like food, travel, or shopping

You can use a mobile app or just a notebook. The method doesn’t matter — consistency does.

Most people don’t realize how much they spend simply because they never track it.

Step 2: Create a Simple Budget

Once you know your spending, the next step is to control it. That’s where a budget helps.

A simple method you can follow is the 50/30/20 rule:

- 50% for essentials

- 30% for personal wants

- 20% for savings and investments

If your income is tight, you can tweak these numbers. The idea is to make sure you’re saving something every month, no matter how small.

You can follow the 50/30/20 budget rule to divide your income effectively and manage expenses.

Step 3: Build an Emergency Fund

Life is unpredictable. Medical expenses, sudden job loss, or urgent needs can come anytime.

That’s why having an emergency fund is important. Try to save at least 3 to 6 months of your basic expenses.

Keep this money in a place where you can access it easily, like a savings account. It acts as a safety net and keeps you from taking loans in tough situations.

Step 4: Save Before You Spend

A simple habit that makes a big difference is saving first and spending later.

As soon as your salary comes in, move a portion of it into savings. Then manage your expenses with what’s left.

If possible, automate this so you don’t have to think about it every month.

Step 5: Start Investing Early

Saving is important, but investing is what helps your money grow.

You don’t need a large amount to begin. Even ₹500 or ₹1000 per month is enough to start.

You can look into options like the following:

- SIPs

- Mutual funds

- Index funds

Starting early gives your money more time to grow, which makes a big difference in the long run.

If you’re earning less, you can still build good habits by following these smart ways to save money even on a low income.

Step 6: Avoid Unnecessary Debt

Debt can be useful in some cases, but it can also become a problem if not handled properly.

Try to avoid spending more than you earn, especially through credit cards. Also, avoid taking loans for things you don’t really need.

If you do use credit, make sure you repay it on time.

Step 7: Focus on Increasing Your Income

There’s only so much you can cut from expenses. At some point, increasing your income becomes important.

You can do this by:

- Learning new skills

- Taking up freelance work

- Exploring small side hustles

Even a small extra income can improve your financial situation.

Common Mistakes to Avoid

Some common mistakes people make in their 20s include:

- Not saving anything

- Spending without planning

- Ignoring investments

- Depending too much on credit

Avoiding these can already put you ahead of many others.

Simple Monthly Plan Example

If you earn ₹20,000 per month, a simple split could look like this:

- ₹10,000 for essentials

- ₹6,000 for personal expenses

- ₹4,000 for savings and investments

It doesn’t have to be perfect. What matters is that you’re saving regularly.

Conclusion

Managing money in your 20s isn’t about being perfect or earning a huge salary. It’s about building small, consistent habits.

Start with what you can, keep it simple, and stay consistent. Over time, these small steps can lead to strong financial stability.